WITHOUT A

WORKERS

COMP CLAIM

orkers’ compensation has existed in Alaska since 1915, but it was not until 1946 that it became compulsory in the state. Workers’ compensation insurance generally gives employers immunity from lawsuits in exchange for covering their employees’ medical costs, missed work, and other expenses related to on-the-job injuries. The employee is not required to prove fault to collect. These no-fault social contracts made the employer liable for work-related injuries and disease regardless of fault.

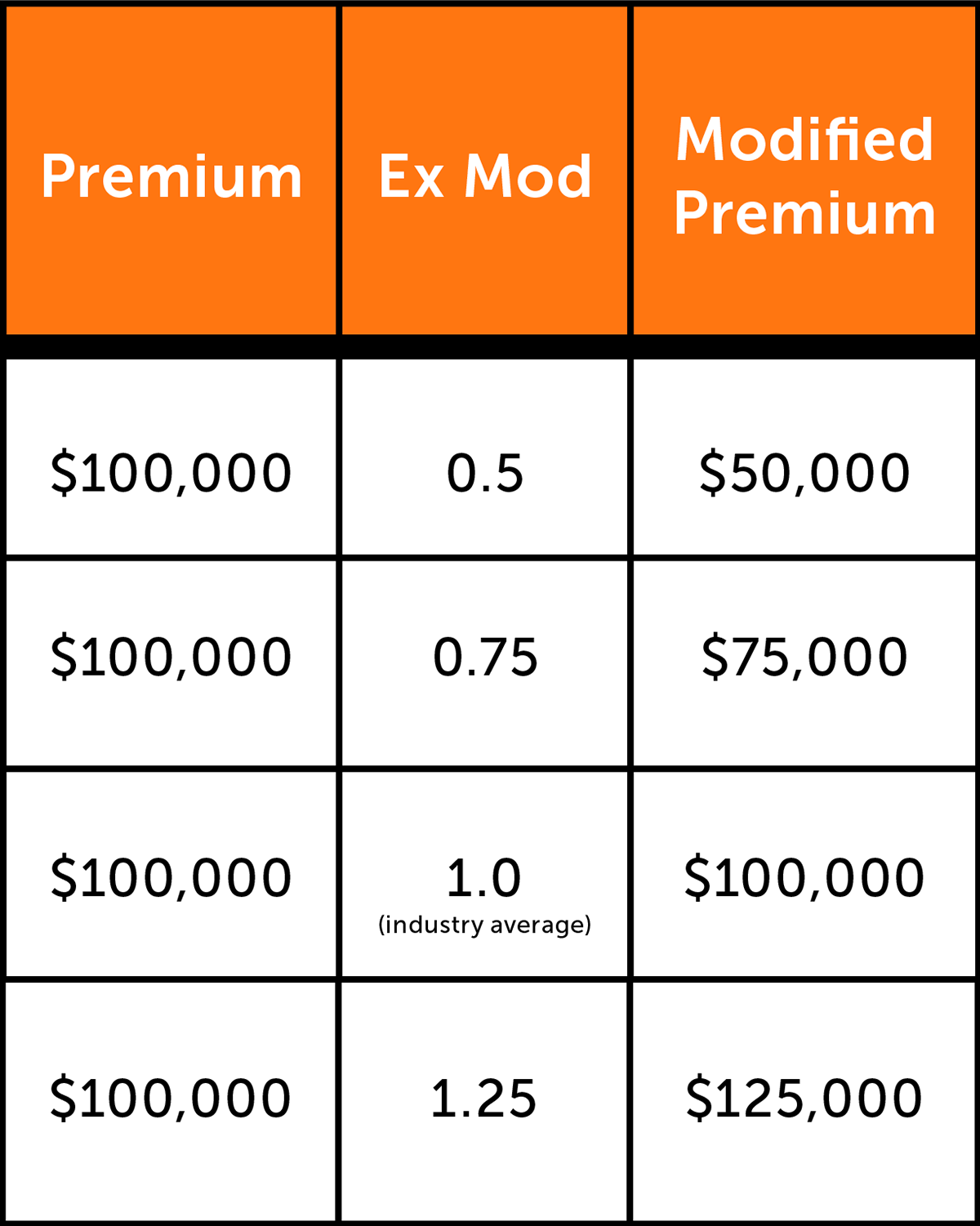

Part of determining how much premium an insurance carrier will require for a workers’ comp policy is the Experience Rating Modification Factor, or Ex-Mod. Insurance carriers use Ex-Mod to describe both past injuries and future risk, which allows carriers to calculate premiums based not only on industry average experience but on each business’ unique operations. This mathematical equation is complicated and often misunderstood but can be best described using this formula: experience modification equals actual losses divided by expected losses.

Since 1947, Alaska has been a member of the National Council of Compensation Insurance (NCCI), which gathers data, analyzes industry trends, and prepares objective insurance rate and loss cost recommendations to insurance carriers. NCCI also creates individual Ex-Mods based on several factors including the payroll of the business, a loss analysis over the last three years, and the class codes for the work being performed. So how can employers reduce these costs?

The simple answer is by controlling exposures that pose a danger to workers. The fewer workers’ compensation claims a business has, the better the Ex-Mod is going to be. Any task that employees are instructed to do on behalf of the business should have a safety plan, hazard analysis, and formal training to protect those employees from hazards they may encounter. While this might sound simplistic, safety is often much more complicated than just hiring a skilled, competent person and giving that person personal protective equipment. Humans are inherently error-prone, and unexpected consequences can strike even the best, most safety-conscious companies. Diligence is key for this approach.

Another strategy to reduce the frequency of injuries is to team up with the insurance carrier to assess loss trends and then specifically target the leading causes of loss. Insurance carriers often have loss control professionals that can create a risk treatment plan customized to a business’s needs. Often these services are free. The business and the insurance carrier (along with the insurance broker) are all partners in risk, after all, and the insurance carrier wants to help the business improve the overall safety of their insured’s operations. This shared goal often reduces risks and improves the safety culture the fastest.

One more option is to train management on the effects of the Ex-Mod on a business’ bottom line. This is helpful in larger companies where owners and managers are ready to work closely together to understand how incident rates drive the Ex-Mod up or down—and how best to implement changes that will drive (or keep) rates down. This is especially useful when a business has a profit-sharing program, where direct savings have tangible results. The Ex-Mod directly affects the premium credit or premium debit assessment that, in turn, affects the cost of insurance. And since the loss experience stays with business for three years, or what is known as the “experience rating period,” it is paramount that officers and managers comprehend how this factor can greatly change how much is paid that year for workers’ comp insurance—and how important it is to work as a team to reduce incidents.

Another time-tested and true tool is claims management. This is a multiple-step approach that starts with reporting the claim as soon as it happens. The longer the claim goes unreported, the higher the probability is that it will cost more. This is due to any number of reasons, but the ones that stand out most are the safety factor and the trust factor. A claim that is reported and properly investigated for root cause(s) in the first three days can often correct the hazard and reduce the future risks to other workers. In addition, the sense of trust between an employee and their employer is a key factor in the outcome of a workers’ comp claim, and this trust is affected if an injury is not addressed promptly. Workers can feel left out, have a morale drop, and worry about the claim process if handled improperly. Statistics show that early reporting of injuries decreases claims costs and helps prevent injury exacerbation, and the worker receives better medical care. It can also reduce the chances of an injured worker “lawyering-up.” By law in Alaska, businesses are required to report injuries within ten days.

The last strategy to reduce the Ex-Mod is implement a return-to-work program. These programs can help an employee stay at work while recovering from their illness or injury. The benefits for the employee include maintaining full earnings, an expedited return to pre-injury work, maintaining of skills, and the contribution to the positive social aspects that working with others brings. For employers, return-to-work increases productivity, reduces administrative costs for substituting workers or paying overtime, and better controls claims costs, to name a few advantages. And since claims costs drive part of the Ex-Mod, this important tool should be part of any employer’s policies. It is best to work with the insurance carrier to formulate and implement these programs.

It is important to note that in many NCCI states—Alaska included—the Experience Rating Adjustment plan is in place, which allows for a 70 percent reduction in the reportable amount of medical-only claims. These are claims where there has been no payment to the worker for lost time, only for medical expenses. This gives employers an incentive to report all claims to their insurance carrier rather than trying to pay for medical-only claims out of pocket. Discounting medical-only claims in the experience modifier calculation greatly reduces the impact of medical-only claims on the modifier. In contrast, Loss Time Incidents have no adjustment in place.

For years Alaska had the highest workers’ comp costs in the nation. That is changing due to an increase in safety and claims management, and as of 2020 Alaska has moved to 10th in the United States. “Reports of injury and occupational illness continue to decrease from a high in 2015,” Alaska Division of Workers’ Compensation Director Charles Collins said in a January 2021 press release. “This is good for workers, good for employers, and good for the economy.”

This really is the bottom line: enhancing worker safety and decreasing risk for all Alaskans. And it saves everyone money, as well. ![]()